StarNuclear Fusion 星核聚变

China’s largest-ever Series A in private commercial fusion — an Integrated Circuit veteran and a Chinese Academy of Sciences plasma physicist join forces in Hefei to pioneer the domestic stellarator route

Hefei StarNuclear Fusion Energy Technology Co., Ltd. (合肥星核聚变能源科技有限公司, hereafter “StarNuclear Fusion”) was incorporated in November 2025 at USTC Silicon Valley (科大硅谷), Hefei High-Tech Zone, Anhui Province, China. Within approximately seven months of its founding, the company closed what is reported to be the largest first-round financing in China’s private commercial fusion sector — RMB 830 million — drawing a consortium of 24 institutional investors spanning industrial capital, nationally-ranked venture firms, and Hefei-based state capital vehicles.

Born in 1981, Dong Wei holds a Bachelor’s degree in Electronic Engineering from Fudan University (复旦大学), one of China’s leading research universities. He subsequently spent approximately two decades in the semiconductor and integrated circuit industry, developing hands-on expertise across precision equipment manufacturing, supply chain management, and industrial capital operations. From 2010 onwards, he pursued a serial entrepreneurship path within the hardware manufacturing sector, leading multiple ventures through their operational and scaling phases. While deeply embedded in the hardware industry, Dong Wei maintained a sustained focus on global energy transition trends, systematically studying fusion energy literature and independently mastering fusion theory. His analytical assessment of the landscape identified a confluence of structural tailwinds: the progressive opening of commercial fusion funding across multiple jurisdictions, the maturation of Hefei’s fusion industrial cluster anchored by EAST and CRAFT (Kuafu), and a near-complete absence of domestic private enterprises focused on the stellarator technical route. Recognising this market whitespace, he founded StarNuclear Fusion in November 2025 at Hefei’s USTC Silicon Valley, anchoring the company’s strategy to a “high-temperature superconducting (HTS) + advanced quasi-isodynamic (QI) stellarator” approach.

A specialist in stellarator magnetic confinement fusion research, Lu Zhiyuan previously served at the Institute of Plasma Physics, Chinese Academy of Sciences (ASIPP, 中国科学院等离子体物理研究所). He holds a doctoral degree from the University of Science and Technology of China (USTC), where his dissertation — “Research on Advanced Stellarator Magnet Physics Optimisation Design” (先进仿星器磁体物理优化设计研究, 2023) — directly addresses the stellarator magnetic configuration design and engineering optimisation challenges at the heart of StarNuclear Fusion’s technical agenda. He and Dong Wei reached alignment on both the stellarator technical route and the engineering commercialisation pathway, forming the company’s founding core.

The pairing of a CEO with two decades of semiconductor and precision manufacturing operational experience with a CTO holding deep academic and applied expertise in stellarator magnet physics directly addresses the dual demands that define deep-tech fusion ventures: scientific credibility and engineering commercialisation capacity. The company notes that ongoing large-device programmes — including ITER and BEST (the Compact Fusion Energy Experimental Device) — have materially elevated China’s fusion engineering capabilities, creating a critical window for advanced stellarator development to transition from research to engineering scale.

StarNuclear Fusion is an early-stage deep-tech company pursuing the engineering and commercial development of magnetic confinement fusion devices on an “HTS + advanced quasi-isodynamic (QI) stellarator” technical platform. As of the Series A close, the company represents the most prominently capitalised domestic private enterprise focused on the stellarator route in China, having secured the largest first-round investment on record in China’s private commercial fusion sector within approximately seven months of incorporation.

Core Technical Pillars:

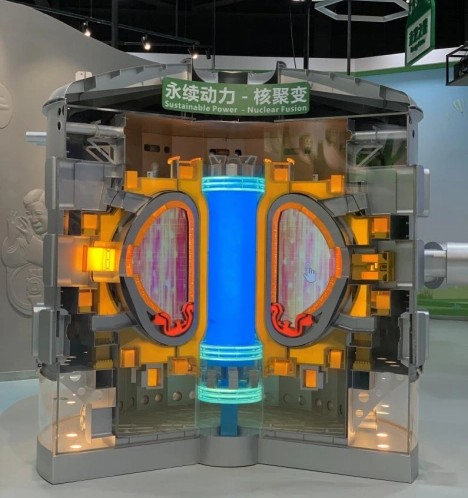

The stellarator’s defining engineering challenge lies in fabricating the complex three-dimensionally twisted coil geometries required to generate the confining magnetic field. StarNuclear Fusion applies HTS magnet technology to this challenge, leveraging HTS materials’ superior magnetic field strength and operational efficiency relative to conventional low-temperature superconductors — materially reducing the cost and manufacturing complexity that have historically constrained stellarator device development timelines.

The QI magnetic configuration targets simultaneous achievement of strong fast-particle confinement and low neoclassical transport — the two principal loss mechanisms that historically limited classical stellarator performance. By engineering precise quasi-isodynamic symmetry into the magnetic geometry, the approach seeks to deliver confinement performance competitive with leading tokamak designs while retaining the stellarator’s intrinsic steady-state operational characteristics.

Because the stellarator sustains its confining magnetic field structure entirely via external coils — without dependence on large plasma currents — it is architecturally immune to the disruptive instability events that represent a key operational constraint in tokamak-based designs. This steady-state characteristic is considered a structural prerequisite for continuous, stable electricity generation in a commercial fusion power station, and is a primary technical motivation for the stellarator route’s renewed commercial interest globally.

Strategic Positioning — First-Mover Advantage in a Structurally Underserved Niche: China’s fusion industry has concentrated investment and talent overwhelmingly on tokamak-based approaches, anchored by state flagship devices. As of StarNuclear Fusion’s founding, no domestic private enterprise had adopted the stellarator as a primary technical focus, leaving the route — and its associated talent pool, supplier relationships, and policy attention — largely uncontested. The company’s entry positions it as the effective domestic first-mover in private stellarator development, with correspondingly lower direct competitive intensity relative to tokamak-focused peers for capital, talent, and strategic partnerships.

StarNuclear Fusion has completed one publicly disclosed financing round since incorporation. The Series A, closed in June 2026, established a post-money valuation of approximately RMB 3 billion and set a new benchmark as the largest known first-round raise in China’s private commercial fusion sector. The composition of the investor syndicate — spanning industrial corporates, nationally-ranked technology venture funds, Hefei municipal state investment vehicles, and a dedicated Hefei fusion-sector fund — reflects a multi-stakeholder validation of the company’s technical thesis across industrial, scientific, and policy dimensions simultaneously.

StarNuclear Fusion was formally incorporated in Hefei’s High-Tech Zone USTC Silicon Valley innovation hub by CEO Dong Wei and CTO Lu Zhiyuan. The company’s strategic focus — “HTS + advanced QI stellarator” — was established at founding. Hefei was selected as the operating base in direct recognition of its unparalleled national fusion infrastructure, comprising EAST, CRAFT, and BEST large-device clusters; an approximately 70-enterprise fusion supply chain; and the operational support ecosystem provided by USTC Silicon Valley’s platform services.

Lead Investors: A four-institution lead consortium comprising SAIC Financial Holdings (上汽金控), Hengxu Capital (恒旭资本), Shenzhen Capital Group (深创投), and CAS Star (中科创星) co-anchored the round. The leads represent a deliberate combination of industrial strategic capital (SAIC Financial), a growth-focused crossover fund, China’s most active state-backed venture manager by deal volume (Shenzhen Capital Group), and a nationally-recognised deep-tech specialist fund affiliated with the Chinese Academy of Sciences (CAS Star).

Follow-On Participants (21 institutions): Chaos Investment (混沌投资), Puhua Capital (普华资本), Dazhou Capital (达晨财智), Legend Star (联想之星, Lenovo Group venture arm), Loongson Venture (龙芯创投), Huakong Fund (华控基金), ZhenFund (钟鼎资本), Fitu Ventures (飞图创投), WestSummit Capital (华登高科), Zijin Mining (紫金矿业, strategic industrial capital), CASVC (国科创投), Zhongding Co. (中鼎股份), GDE Capital (粤科创投), Nanshan Strategic Emerging Industries Fund (南山战新投), Jingkai Capital (晶凯资本), Yunze Capital (云泽资本), Yihua Capital (益华资本), Zero2IPO Holdings (清科控股), Fenghe Capital (峰和资本), Hefei Innovation Investment (合肥市创新投), and Hefei Hi-Tech Investment (合肥高投).

Capital Composition Analysis: The round is notable for the simultaneous participation of three structurally distinct capital categories — industrial corporates with direct sector alignment (Zijin Mining), nationally-ranked deep-tech specialist venture funds (CAS Star, Shenzhen Capital Group), and Hefei municipal government investment vehicles (Hefei Innovation Investment, Hefei Hi-Tech Investment). This tri-layer composition provides StarNuclear Fusion with simultaneous validation across industrial, scientific, and policy dimensions, and is expected to materially strengthen access to supply-chain partnerships, R&D infrastructure, and government support mechanisms in subsequent development phases.

StarNuclear Fusion’s competitive positioning rests on four structural pillars: first-mover status on the domestic stellarator route, a complementary founding team bridging industrial engineering and plasma physics, co-location within China’s foremost fusion industrial cluster, and a capital structure that simultaneously engages industrial, national-level venture, and municipal government capital. Given the pre-commercial nature of the business, these advantages are assessed on their capacity to sustain the company through the technology validation cycle rather than on near-term revenue metrics.

China’s fusion investment landscape has concentrated overwhelmingly on tokamak-based approaches, anchored by nationally-funded flagship devices. At the time of StarNuclear Fusion’s founding, no domestic private enterprise had established a primary focus on the stellarator technical route. This whitespace entry provides the company with structurally lower direct competitive intensity for talent recruitment, supplier relationships, and investor attention compared with tokamak-focused peers, and positions it as the reference entity as domestic stellarator interest accelerates globally.

CEO Dong Wei brings two decades of semiconductor and precision manufacturing operational experience — covering equipment, supply chain, and capital operations — that is directly transferable to the industrialisation of complex fusion hardware. CTO Lu Zhiyuan’s doctoral research at USTC under ASIPP advisement, specifically on advanced stellarator magnet physics optimisation, provides the scientific foundation for the company’s core technical differentiation. The combination addresses the two failure modes most common to deep-tech fusion ventures: insufficient scientific rigour, and inability to translate validated science into manufacturable engineering.

Hefei hosts China’s most concentrated fusion science and industrial infrastructure: EAST, CRAFT (Kuafu), and BEST large-scale experimental devices; approximately 70 enterprises covering the full fusion value chain from superconducting materials and core magnets to main device equipment and engineering construction. Hefei’s 14th Five-Year Plan explicitly targets commissioning of a compact fusion energy experimental device and construction of a dedicated fusion science and technology demonstration zone (Jubian Chuangke Shifanqu, ~23,000 mu). Two dedicated university fusion engineering faculties were simultaneously inaugurated in January 2026, establishing a localised talent pipeline that serves the company’s medium-term recruitment requirements.

The Series A syndicate’s simultaneous participation of industrial corporates (Zijin Mining), nationally-ranked deep-tech venture funds (CAS Star, Shenzhen Capital Group), and Hefei municipal state investment vehicles (Hefei Innovation Investment, Hefei Hi-Tech Investment) constitutes a form of multi-stakeholder validation rarely achieved in a first-round close. This capital architecture is strategically significant beyond its financing function: industrial investors signal supply-chain and off-take alignment; state venture funds signal national technology priority endorsement; and municipal capital signals privileged access to local policy support, land, and infrastructure resources in subsequent development phases.

The Stellarator’s Moment — Global Tailwinds Converging: The stellarator technical route has entered a period of materially improved commercial viability, driven by convergent advances across computation (AI-accelerated QI magnetic configuration design), manufacturing (precision 3D printing enabling complex coil geometry fabrication at scale), and materials (HTS enabling stronger magnetic fields at lower operational cost). Internationally, Type One Energy (acquired by Realta Fusion), Renaissance Fusion, and Proxima Fusion are among the ventures pursuing stellarator commercialisation with institutional backing. In China, StarNuclear Fusion’s emergence alongside parallel activity at Yanfusion (岩超聚能) — which commissioned China’s first stellarator 3D superconducting magnet production line in Q1 2026 — signals the beginning of a dedicated domestic stellarator investment ecosystem.

StarNuclear Fusion is a pre-commercial deep-tech venture at the earliest stage of its development lifecycle. The analytical framework appropriate for evaluating its risk-return profile differs materially from that applicable to revenue-generating growth companies: near-term value creation is driven by technology validation milestones, team credibility, and ecosystem positioning rather than financial performance metrics. The following assessment reflects the publicly available information as of the Series A close in June 2026.

- Structural whitespace in China’s private fusion sector creates first-mover positioning on the stellarator route with limited direct domestic competition at the time of entry.

- Global stellarator commercial interest is accelerating in parallel with HTS magnet maturation, 3D printing fabrication advances, and AI-driven QI configuration optimisation — providing a technology readiness tailwind.

- Hefei’s state-endorsed fusion industrial cluster and dedicated municipal investment infrastructure provide privileged access to supply chain, talent, and policy support mechanisms not available to ventures operating in less concentrated geographies.

- The tri-layer capital structure (industrial + national VC + municipal state capital) positions the company for smoother access to follow-on financing and non-dilutive government grant support in subsequent development phases.

- Global commercial fusion market potential is substantial: successful development of a commercial fusion power plant would represent one of the largest addressable energy markets in history, providing a correspondingly large return surface for early-stage investors with the risk tolerance and time horizon to hold through the development cycle.

- Technology development uncertainty is the primary risk: fusion engineering across all routes is characterised by high R&D complexity and long development timelines, and the stellarator’s shorter domestic engineering commercialisation track record amplifies this uncertainty relative to tokamak-focused peers.

- Commercial pathway opacity: the roadmap from the current pre-device stage to grid-connected power generation — and the economics of that pathway — remains unvalidated and subject to material revision as engineering milestones are encountered.

- Competitive escalation: China’s fusion sector is experiencing a marked acceleration of capital deployment across multiple technical routes simultaneously. The stellarator whitespace that StarNuclear Fusion occupies today could attract additional well-capitalised entrants as the route gains visibility, particularly if early technical milestones validate the approach.

- Governance and control complexity: the concurrent participation of Hefei municipal state capital, policy-aligned funds (Hefei Future Fusion Energy Venture Fund), and multiple institutional investors introduces potential for governance complexity and misalignment of objectives in future strategic decisions, particularly regarding internationalisation or strategic partnership formation.

- Information disclosure limitations: as an early-stage, non-listed Chinese private company, publicly available technical, operational, and financial data is limited. The figures cited herein are derived from media reporting and should be treated as indicative pending independent verification via direct due diligence.

Investors evaluating StarNuclear Fusion should apply an analytical framework appropriate to pre-commercial deep-tech ventures rather than conventional venture or growth equity metrics. The company’s current value proposition rests entirely on the quality of its technical differentiation, team composition, ecosystem positioning, and capital access — none of which generate near-term revenue or can be stress-tested via financial statement analysis. A minimum 10-15 year investment horizon should be assumed for any exposure to commercial fusion sector ventures at this stage of development.