FINN

Germany’s leading car subscription platform — the Munich-born mobility challenger that became a unicorn in seven years

FINN is a car subscription (“Auto Abo”) platform founded in 2019 in Munich, Germany, by six co-founders: Max-Josef Meier, Maximilian Wühr, Nikolai Schröder, Andreas Stryz (also referenced as Andreas Wixler in early public materials), Max Beyer, and Hans-Peter Ringer. The founding motivation is generally described along two lines. Inaugural CEO Max-Josef Meier was driven by ambitions to build a large-scale e-commerce venture, while co-founder Maximilian Wühr’s conviction stemmed from a frustrating and opaque car-buying experience in the San Francisco Bay Area in the United States. This experience crystallized into the company’s core motto: “if you can order a sofa online, why not a car?”

All founding members connected through a private network centered on Munich’s Ludwig Maximilian University (LMU) and the Center for Digital Technology and Management (CDTM), assembling a team whose professional backgrounds were deliberately complementary. Max-Josef Meier was a co-founder of the e-commerce startup Stylight and an active angel investor, including in Personio, while Maximilian Wühr built his business-development experience at health-tech company Kaia Health and venture firm Picus Capital. Max Beyer spent six years at Boston Consulting Group (BCG), rising to Principal; Nikolai Schröder is likewise a BCG alumnus; and Hans-Peter Ringer is an industry veteran who spent more than eight years at rental-car company Sixt, most recently heading international fleet purchasing. CTO Andreas Stryz (cited as Andreas Wixler in early launch materials) previously led consumer-product software development at the online home-furnishings company Westwing.

Studied economics at LMU Munich and Bocconi University in Italy. Prior business-development experience at Kaia Health and as an investment professional at Picus Capital. Served as Chief Growth Officer and head of the U.S. market before being appointed CEO in April 2023. Graduated secondary school early at age 17 and emerged as the leader of an organization several hundred employees strong before age 30.

Co-founder of e-commerce startup Stylight and an active angel investor, including in Personio, with a track record as a serial entrepreneur. Led FINN for four years and drove its early growth, but stepped down from management by mutual agreement in 2023 following allegations of sexual harassment.

FINN’s board includes prominent investor-side figures such as HV Capital partner Rainer Märkle, who joined the board at the company’s founding in 2019, and Nathan Medlock of Planet First Partners, who led the 2024 Series C round. In April 2023, an internal leadership transition took place within the founding group: Max-Josef Meier stepped down after a four-year tenure as CEO, with co-founder and then-Chief Growth Officer Maximilian Wühr appointed as the new CEO, Chief Fleet Officer Jürgen Lobach (who had joined in 2020) elevated to the management team, and then-CFO Max Beyer remaining in his role. Max Beyer subsequently left the company voluntarily at the end of 2024 to spend more time with his newborn child, and in October 2025 Florian Drabeck — a finance veteran who successfully led the IPOs of Westwing and Tonies — joined as the new CFO, where he is now leading efforts to strengthen the company’s financial infrastructure with a potential future listing in mind.

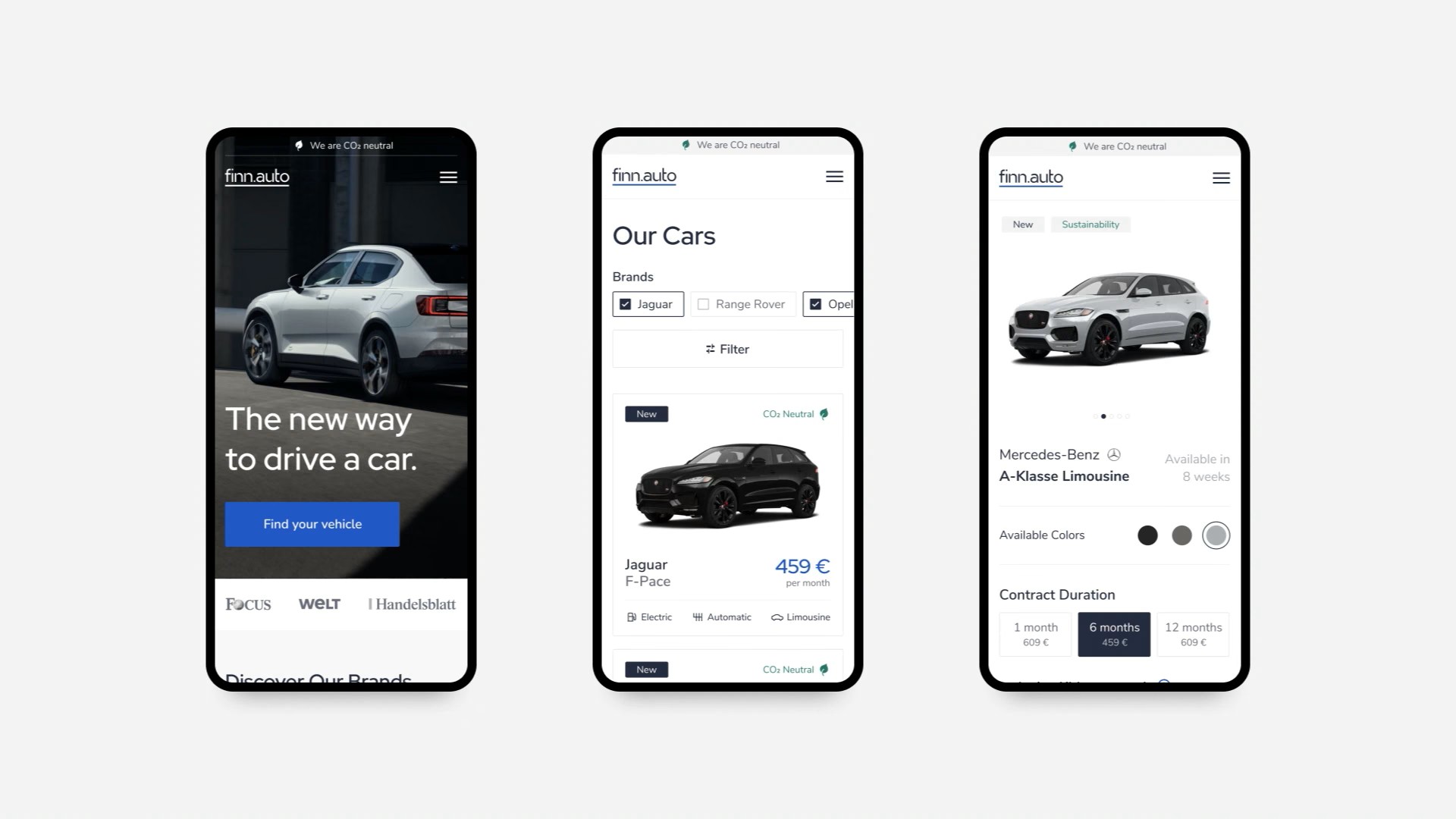

FINN’s core business model is the “all-inclusive car subscription.” Customers select a new car online from more than 30 brands and have it delivered to their door, paying a single monthly subscription fee that bundles insurance, registration tax, vehicle tax, maintenance, and damage coverage. Contract terms range from six to 24 months with no down payment or hidden fees; the customer’s only separate cost is fuel or charging. This structure lowers the barrier to entry relative to traditional car purchase or leasing, while the company itself absorbs the risk associated with fluctuations in residual value.

| Business Area | Status | Stage | Notes |

|---|---|---|---|

| Germany B2C Subscription | Nationwide service, 50,000+ active subscriptions | Market Leader | 30+ brands including BMW, Mercedes-Benz, Opel, Hyundai; processes 200–300 deliveries per month |

| B2B Fleet / JobAuto | Expanded to roughly half of total ARR | High Growth | Corporate fleet subscriptions and the JobAuto employee-benefit product have become a core growth driver |

| U.S. Operations | Serves 11 Eastern states plus Washington, D.C.; expansion paused | Selective Operation | Capital-intensive expansion halted as of February 2024 in favor of a German core-market focus |

| Chinese OEM Partnerships | Up to 5,000 BYD units (June 2025), 1,000 Great Wall Motor units, and others | Expanding | Serves as a key distribution channel for BYD’s entry into the German private market |

| Electrification Transition | EV / PHEV share roughly 35–40% | Targeting | Goal of raising the share of EVs and low-emission vehicles to over 80% by 2028 |

Strategic Re-Prioritization (February 2024): FINN formally announced that it would prioritize sustainable growth in its German core market and fleet electrification over capital-intensive international expansion. This marked a clear pivot away from the aggressive overseas-expansion strategy pursued since entering the U.S. East Coast in 2022, toward a profitability-oriented approach — a shift reflected in the CEO’s repeated emphasis on “profitable growth” around the Series D round.

From its initial capital raise in late 2019 through its Series D in June 2026, FINN has raised approximately €250 million (roughly $250–260 million) in cumulative equity funding, in addition to separately securing more than $1 billion in cumulative debt-based fleet financing through asset-backed securities (ABS) and related structures. Notably, each successive round has aligned with the achievement of a preceding operational milestone — U.S. market entry, the shift toward B2B, and accelerated electrification — and the investor base has globalized over time, from early German local investors to Canadian fintech-focused investment firm Portage.

An early round completed shortly after incorporation, used to validate the business model with a fleet of roughly 75 vehicles and around 1,000 subscriptions sold.

Led by White Star Capital. Existing shareholders Heartcore, HV Capital, Picus Capital, and UVC Partners participated, alongside individual investors including Zalando co-founders Rubin Ritter, David Schneider, and Robert Gentz. The round secured FINN’s first wave of institutional backing, laying the groundwork for fleet expansion and team growth.

Led by Korelya Capital (backed by South Korea’s Naver). Keen Venture Partners, Climb Ventures, Greentrail Capital, and Waterfall Asset Management joined as new investors. Proceeds funded entry into the U.S. East Coast (New Jersey, Pennsylvania, and others) and the opening of a New York headquarters. Around the same time, FINN separately secured up to $720 million in ABS debt financing from Credit Suisse and Waterfall.

Led by Planet First Partners, a European sustainability-focused growth-equity investor, with Nathan Medlock joining the board. HV Capital, Korelya Capital, UVC Partners, White Star Capital, and Picus Capital all participated strongly as existing investors. Proceeds were earmarked to raise the EV/PHEV share of the fleet from 40% to over 80% by 2028. ARR reached €160 million and active subscriptions crossed 25,000 around this time.

A new asset-backed securities (ABS) program, “ABS II,” arranged by Citi and Jefferies, with Avellinia Capital participating. This debt-based structure, secured against the vehicle fleet itself, funds fleet expansion without equity dilution. Cumulative debt-based financing expanded to more than €1 billion.

New lead investment from Portage, a Canadian fintech- and mobility-focused investment platform. Early investor UVC Partners substantially increased its commitment, while Planet First Partners, Korelya Capital, White Star Capital, HV Capital, and Picus Capital all re-participated as existing investors. BC Partners Credit and Runway Growth Capital provided more than €40 million in additional debt financing. SevenVentures, the investment arm of ProSiebenSat.1, participated via a media-for-equity structure, granting FINN access to large-scale advertising inventory. Jefferies acted as placement agent for the round. This round pushed FINN’s valuation above €1 billion for the first time, admitting it to Germany’s unicorn club.

The European car subscription market was valued at approximately $3.91 billion in 2025 and is projected to grow at roughly 25% annually to reach $35.95 billion by 2035 — a high-growth category in which Germany represents about 34% of total demand, making it FINN’s most important market. Competitors in this space include Sixt’s subscription brand “Sixt+,” Stellantis’s “Free2Move,” the UK-based EV-focused platform Onto, and Volvo’s “Care by Volvo.” Cluno, once FINN’s largest independent German rival, was acquired by ViveLaCar, which was in turn absorbed by The Platform Group in 2023 and now operates with fewer than ten employees. Within this landscape, FINN’s structural points of differentiation include the following.

FINN has established itself as Germany’s leading car subscription provider seven years after its 2019 founding, with more than 50,000 active subscriptions and over €300 million in ARR — a scale that dwarfs other independent startups. While rival independents such as Cluno have consolidated and shrunk, FINN has continued to expand its economies of scale.

Framework agreements with Stellantis (11,500 units), Hyundai (5,000 units), BYD (up to 5,000 units), and Great Wall Motor (1,000 units), among others, secure a stable, high-volume vehicle supply chain. For new Chinese-brand entrants, FINN serves as a key distribution channel into the German private market, giving it outsized negotiating leverage.

Corporate subscriptions and the employee-benefit “JobAuto” product now account for roughly 50% of ARR and have become a core growth engine. Compared with B2C, B2B contracts carry higher per-account value and lower churn, contributing simultaneously to margin improvement and revenue stability.

An asset-backed securities structure collateralized by the vehicle fleet itself has enabled FINN to raise more than €1 billion in cumulative debt financing without equity dilution. Backing from global investment banks such as Citi and Jefferies gives FINN an edge over competing startups in cost of capital and speed of expansion.

Subscriptions let consumers experience an EV short-term without the technological-obsolescence or residual-value risk of long-term ownership. The 2028 target of 80% electric/low-emission fleet share aligns with EU carbon-neutrality policy direction and has attracted ESG-oriented capital, including Article 9 funds such as Planet First Partners.

A media-for-equity agreement with ProSiebenSat.1’s SevenVentures grants FINN access to large-scale advertising inventory without cash outlay. The company already generates 60% of its subscriptions from organic traffic, reflecting strong existing brand awareness; this deal functions as a cost-efficient marketing lever for reaching the next wave of mass-market consumers.

What Portage’s Lead Investment Signals: The decision by Portage — a fintech- and mobility-focused investment platform with more than $6.3 billion in assets under management, part of Sagard — to lead the Series D round is a signal that extends beyond simple capital-raising. Portage’s prior portfolio has centered on fintech companies such as Wealthsimple, Marshmallow, and auxmoney, suggesting an investment thesis that frames FINN as a “mobility fintech with a subscription-based payment and asset-management model.” This implies that FINN is increasingly being re-rated not as a simple car-rental business, but as a financial and subscription enterprise.

As of its June 2026 Series D, FINN remains a privately held unicorn, and specific profitability figures — net margin, EBITDA, and similar metrics — have not been disclosed in publicly available materials. Management has repeatedly emphasized “profitable growth,” and past executive commentary has noted that “the core product is profitable,” but whether the company has achieved company-wide profitability has not been explicitly disclosed and remains a data gap. The October 2025 hiring of Florian Drabeck, a CFO with extensive IPO experience, can be read as a signal of financial-infrastructure preparation with a future listing in mind; however, investor commentary (from HV Capital) has explicitly noted that “there is no near-term pressure to execute,” leaving the specific timing of any IPO uncertain.