Alebund Pharmaceuticals

China’s first vertically integrated renal innovation platform — from Lilly Asia Ventures incubation to HKEX Main Board listing, commanding the broadest CKD pipeline coverage in its peer group

Alebund Pharmaceuticals (Jiangsu) Limited was established in early 2018 in Shanghai as a renal-focused biopharmaceutical enterprise co-incubated by Lilly Asia Ventures (LAV) and a consortium of nephrology thought leaders. Headquartered in Yangzhou, Jiangsu Province, the company is principally engaged in the discovery, development, manufacture, and commercialization of innovative therapies for chronic kidney disease (CKD) and its associated complications. Alebund distinguishes itself as a vertically integrated platform — encompassing proprietary GMP manufacturing, a dedicated nephrology salesforce, and a wholly-owned drug pipeline — structured from inception to progress candidates from bench to commercial launch without dependence on external partners for core functions.

PhD, University of Chicago. A seasoned entrepreneur and healthcare investor with over 15 years of cross-functional experience spanning drug discovery, venture capital, and executive management of biopharmaceutical startups. Prior to Alebund, Dr. Xia served in strategic and investment roles at Navigant Consulting (NYSE: NCI), Eli Lilly’s Asia Fund, and AbbVie (2256.HK). He joined Alebund’s board as a Director representing LAV before transitioning to CEO in November 2018. Undergraduate, Peking University.

Master’s degree in Nephrology, Second Military Medical University (SMMU), PLA Navy. Postdoctoral research in Internal Medicine, Yale School of Medicine. Prior clinical development roles at Abbott Laboratories and Roche, with a focus on renal therapeutic development. Dr. Tian is the scientific originator of lead asset AP301, having co-founded Vidasym Inc. — the U.S.-based entity in which AP301 was first developed — before transitioning global rights to Alebund. Fellow, American Society of Nephrology (FASN).

The Board is further strengthened by Dr. Huading Zhang (PhD, scientific oversight), Ms. Yun Wang (operations), and independent non-executive director Dr. Marietta Wu (MD, PhD, MBA; affiliated with Quan Capital), collectively providing a balance of clinical, scientific, and capital markets expertise. The LAV incubation model — extending beyond capital provision to encompass scientific co-direction and founding team assembly — represents a structurally rare starting point that embedded deep domain expertise into the company’s architecture from day one.

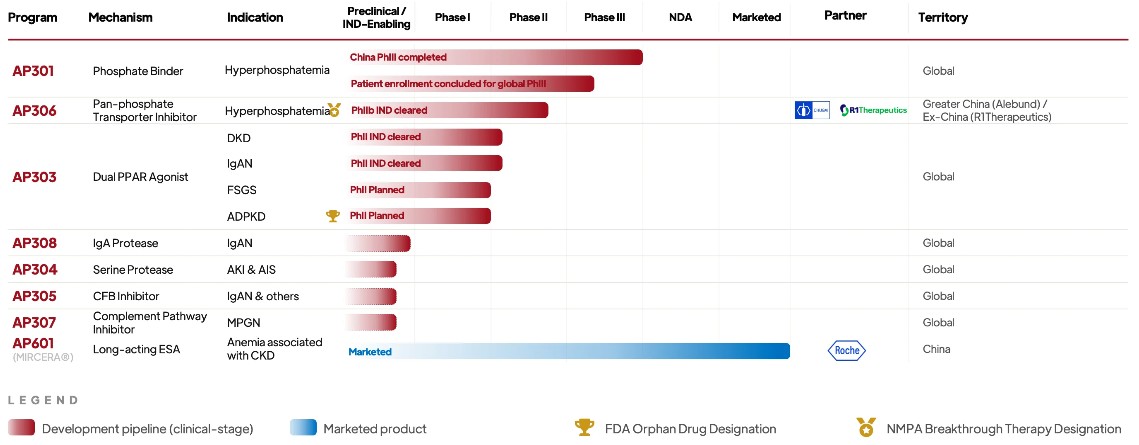

Alebund’s strategic architecture is defined by a deliberate tension between focus and diversification: unwavering concentration on the renal therapeutic area, paired with intentional spread across indication, mechanism, and modality. As of the June 2026 HKEX listing, the company holds one commercialized product (Mircera®) and seven pipeline candidates — a breadth of renal indication coverage that management asserts is unmatched among pure-play kidney-focused biopharmaceutical companies globally. The pipeline spans both small-molecule and biologic modalities, encompassing first-in-class and best-in-class assets across CKD complications, immunologic nephropathy, metabolic kidney disease, and rare renal disorders.

| Asset | Indication | Stage | Key Details |

|---|---|---|---|

| Mircera® | Renal Anemia (CKD) | Commercialized | Long-acting ESA (erythropoiesis-stimulating agent). Marketed via Alebund’s proprietary nephrology salesforce in China. Generates near-term revenue while building commercial infrastructure ahead of AP301 launch. |

| AP301 | Hyperphosphatemia in dialysis-dependent CKD | Phase 3 | Best-in-class oral iron-based phosphate binder. China Phase III primary endpoint met. China-U.S. Phase III MRCT fully enrolled. NMPA NDA submission imminent. Potential first oral iron-based phosphate binder approved in China. |

| AP306 | Hyperphosphatemia (dialysis & non-dialysis CKD) | Phase 2 | First-in-class pan-phosphate transporter inhibitor. NMPA Breakthrough Therapy Designation (BTD) granted. Ex-Greater China rights licensed to R1 Therapeutics (March 2026). Phase II efficacy data markedly superior to sevelamer. |

| AP303 | DKD / IgAN / ADPKD | Phase 2 (Pending) | First-in-class dual PPAR agonist. Favorable Phase I safety profile in healthy volunteers and DKD patients (Australia & China). IND cleared by both FDA and NMPA. Basket Phase II trial in DKD/IgAN planned H2 2026. FDA ODD for ADPKD secured. |

| AP308 | IgA Nephropathy (IgAN) | Pre-IND | First-in-class engineered recombinant IgA protease targeting functional cure of IgAN via enzymatic cleavage of galactose-deficient IgA1. IND submissions to both FDA and NMPA planned Q3 2026. |

| AP303 (ADPKD) | Autosomal Dominant Polycystic Kidney Disease | Rare Disease Designation | FDA Orphan Drug Designation (ODD) obtained. Expanding indication scope of AP303 platform into rare renal disease with regulatory exclusivity incentives. |

Vertical Integration Advantage — Proprietary GMP Manufacturing: Alebund’s small-molecule GMP production facility in Yangzhou, Jiangsu has been completed and is fully operational, holding a Drug Manufacturing License (Category B) issued by the Jiangsu Provincial Drug Administration. This infrastructure positions the company for a direct transition from NMPA NDA approval to commercial-scale production of AP301 without dependence on external contract manufacturers — eliminating a key supply-chain risk that affects many asset-light peers. The co-located nephrology salesforce, already active in promoting Mircera®, provides a pre-built commercial channel for AP301’s anticipated launch.

The world’s first and only clinical-stage pan-phosphate transporter inhibitor, operating via an entirely distinct mechanism from conventional phosphate binders — suppressing intestinal phosphate absorption at the transporter level rather than binding phosphate in the gut lumen. Phase II data demonstrate superiority over sevelamer carbonate with approximately 95% of patients achieving target serum phosphate versus approximately 50% for the active comparator. Ex-Greater China rights out-licensed to R1 Therapeutics, sharing global development risk and capital.

A differentiated dual PPAR (α/γ) agonist designed to simultaneously attenuate renal fibrosis and inflammation — the two convergent pathways driving CKD progression across multiple etiologies. By targeting a shared downstream mechanism, AP303 is being pursued as a basket program in DKD, IgAN, and ADPKD via a single Phase II protocol, an efficient design that reduces per-indication development costs. Phase I demonstrated a clear dose-dependent PD signal and favorable safety in both healthy volunteers and DKD patients.

A first-in-class engineered recombinant protease that cleaves galactose-deficient IgA1 (Gd-IgA1) — the etiologic agent of IgAN — at its hinge region, offering a mechanistically distinct approach oriented toward durable disease modification or functional cure rather than symptomatic management. Represents one of the most scientifically differentiated assets in the Alebund pipeline, with a clear biological rationale and no approved precedent for enzymatic IgA cleavage.

An oral iron-based phosphate binder offering superior phosphate binding capacity relative to calcium carbonate- and polymer-based comparators, with the ancillary benefit of addressing concurrent iron deficiency anemia common in dialysis populations. The dual phosphate-binding and iron-supplementing profile differentiates AP301 from single-purpose binders. China Phase III primary endpoint has been met, with MRCT enrollment completed across Chinese and U.S. sites, advancing the asset toward potential dual-market regulatory filings.

Since its 2018 inception, Alebund has executed seven discrete external financing rounds, raising approximately US$335 million in pre-IPO capital across a progressively diversified institutional investor base. The June 2026 HKEX Global Offering added approximately HK$1.283 billion (~US$164 million) in gross proceeds, bringing total cumulative funding to approximately RMB 2.0 billion. A consistent feature of Alebund’s capital formation is milestone-triggered progression: each successive round has been anchored to the attainment of a discrete clinical or regulatory benchmark, maintaining credibility with institutional allocators and reducing valuation dilution risk. Investor composition has evolved systematically from specialist healthcare venture capital (LAV, Quan, Sherpa) through global multi-strategy hedge funds and sovereign wealth to cornerstone participation by GIC and Tencent at IPO.

Lilly Asia Ventures co-incubated Alebund alongside a group of senior nephrology practitioners, in what constitutes a structured NewCo formation rather than a conventional venture investment. LAV’s role extended to scientific co-direction, founding team assembly, and initial pipeline architecture — establishing a distinctive starting point relative to typical startup configurations. Dr. Gavin Xia joined as an LAV-designated Director before converting to CEO in November 2018, creating a governance structure that aligned the lead investor and executive management from inception.

Huagai Capital (华盖资本) and Med-Fine Capital (联新资本) co-led Alebund’s first formal institutional financing round, with Lilly Asia Ventures participating as a follow-on investor. Proceeds were directed toward early-stage development of AP301 and initial organizational build-out. Med-Fine Capital, known for its NewCo incubation expertise across the Chinese healthcare sector, reinforced the venture creation thesis underpinning Alebund’s founding architecture.

Quan Capital led a US$60 million Series B, joined by a prominent sovereign wealth fund, 3E Bioventures Capital, Sherpa Healthcare Partners, and existing shareholders Lilly Asia Ventures and Med-Fine Capital. At the time, this represented the largest single financing round raised by any nephrology-dedicated biopharmaceutical company in China. The capital was deployed across AP301 Phase II clinical execution, commencement of the Yangzhou manufacturing facility construction, and pre-clinical pipeline expansion. Quan Capital’s participation — a firm with deep China healthcare investment expertise and global reach across Shanghai, Menlo Park, and Boston — materially elevated Alebund’s institutional credibility.

3H Health Investment, Loyal Valley Capital, and Morningside Ventures co-led a US$54.5 million Series B+, with YuanBio Venture Capital, Octagon Capital, Verition Fund Management, and HT Capital joining as new investors. All existing institutional shareholders re-upped, underscoring durable conviction. Critically, this round closed concurrent with Alebund’s execution of an option and license agreement with Chugai Pharmaceutical (a Roche Group affiliate) for AP306, providing external validation of the company’s scientific and commercial credibility from a major global pharmaceutical group. Proceeds accelerated AP301 Phase III initiation, the Yangzhou facility, and AP306 development.

Yangzhou Guojin Investment Group (扬州国金投资集团, state-owned) and Yangzhou Longchuan Holdings co-led a Pre-Series C financing of approximately RMB 200 million. The participation of state-affiliated capital from the municipality hosting Alebund’s manufacturing operations formalizes the company’s strategic positioning in Yangzhou and reflects local government alignment with its commercial ambitions. Concurrently, Alebund secured a RMB 800 million syndicated loan credit facility from banking partners, demonstrating access to non-dilutive debt financing alongside equity.

An undisclosed prominent healthcare fund, Yangzhou Guojin Investment Group, and Kingray Capital (晶泰资本) participated in a RMB 550 million Series C first close, establishing a post-money valuation of approximately RMB 3.779 billion. This round served as the final private capital raise prior to the HKEX listing, providing the balance sheet runway to advance AP301 toward NDA submission, fund the AP306 U.S.-China Phase II trial, and support expanded commercialization of Mircera®. The closing of Series C in a challenging broader biotech financing environment underscored sustained investor conviction in the renal platform thesis.

Alebund priced 56,755,400 H Shares at HK$22.60 per share (5,675,600 under the Hong Kong public offering; 51,079,800 under the international offering). Gross proceeds totaled approximately HK$1.283 billion, expandable to approximately HK$1.475 billion (~US$189 million) upon full exercise of the over-allotment option (8,513,300 shares).

Cornerstone investors committed approximately US$81.5 million (~HK$639 million), representing 49.78% of the total offering: GIC (Singapore sovereign wealth fund), Loomis Sayles, RTW Investments, SymBiosis, Tencent, Cormorant Asset Management, Dymon Asia, GF Fund, China Universal Asset Management, E Fund, and Loyal Valley Capital. The international tranche was approximately 19.77 times oversubscribed; the Hong Kong public tranche approximately 963.56 times oversubscribed. Shares closed the first trading day at HK$46.00, representing a 103.54% premium to the offer price.

The global phosphate management landscape includes Vifor Pharma’s Velphoro (sucroferric oxyhydroxide), Akebia Therapeutics’ HIF-PH inhibitors for renal anemia, and Travere Therapeutics’ sparsentan for IgAN, while the Chinese renal drug market features domestic players across adjacent categories. Alebund’s competitive defense derives not from any individual asset but from the integrated platform structure — a concentration on a single therapeutic area combined with diversification across indication, mechanism, and regulatory geography — that generates a compounding moat rather than a single-point advantage.

Six or more distinct renal indications addressed across one commercialized product and seven pipeline candidates — a portfolio breadth unmatched among pure-play renal biopharmaceutical companies. This structural diversification distributes single-asset failure risk while enabling a unified nephrology salesforce to commercialize multiple products through a single channel, generating material operating leverage relative to indication-specific peers.

AP301 is advancing China NMPA NDA filing concurrently with a fully enrolled China-U.S. Phase III MRCT — a rare dual-geography registration strategy for a China-originated asset. AP303 holds cleared INDs from both the FDA and NMPA, while AP306’s ex-Greater China rights have been licensed to R1 Therapeutics, distributing global development capital and risk. This regulatory architecture positions Alebund as a genuine global clinical-stage company rather than a China-domestic operator.

The Yangzhou small-molecule GMP facility is operational and licensed (Drug Manufacturing License, Category B, Jiangsu Provincial Drug Administration). Upon NMPA approval of AP301, Alebund can transition directly to commercial-scale production without CMO dependency — eliminating supply-chain risk that has historically caused post-approval launch delays for asset-light peers. The integrated manufacturing capability also supports tighter cost-of-goods management over the product lifecycle.

AP301 (best-in-class phosphate binder) reduces regulatory and clinical risk through a validated mechanism; AP306, AP303, and AP308 (all first-in-class) command premium pricing, exclusivity, and partnership optionality. This deliberate portfolio balance distributes risk-reward across the value creation spectrum: the best-in-class assets provide near-term NDA visibility while the first-in-class candidates represent differentiated long-duration upside, including potential M&A optionality from global pharmaceutical acquirers.

Approximately 76% of Chinese dialysis patients fail to achieve target serum phosphate levels, versus 52% in the U.S. and 39% in Japan — a treatment gap that is structural, not cyclical, reflecting formulary limitations rather than access barriers. With 9.2 million hyperphosphatemia cases in China (out of 80.2 million globally in 2024), an NMPA approval for AP301 would insert a differentiated oral agent into a market with documented high unmet need and a captive dialysis patient population with limited existing options.

The participation of Singapore’s GIC and Tencent as cornerstone investors — accepting a minimum six-month mandatory lock-up — constitutes a formal, public endorsement of Alebund’s long-term value thesis by two of Asia’s most credible institutional allocators. Loyal Valley Capital’s re-participation at the IPO after leading the Series B+ underscores durable investor conviction across the capital structure. This quality of cornerstone composition is atypical for a pre-NDA biopharmaceutical listing and confers ongoing institutional credibility in secondary market trading.

Strategic Significance of the Chugai / AP306 License: AP306 was originally developed by Chugai Pharmaceutical, a Roche Group affiliate, as EOS789 — a pan-phosphate transporter inhibitor for hyperphosphatemia. Alebund acquired global development and commercialization rights via an option-exercise in July 2021, subsequently sublicensing ex-Greater China territories to R1 Therapeutics in March 2026. The willingness of a major Japanese pharmaceutical group to out-license a clinically validated, first-in-class mechanism to a China-based operator of Alebund’s scale represents an implicit endorsement of both the asset’s potential and Alebund’s execution capability in the renal space. The sublicense to R1 Therapeutics further demonstrates capital-efficient portfolio management — retaining China rights while distributing ex-China risk and cost.

As of its June 2026 HKEX listing, Alebund occupies a hybrid position: it generates commercial revenue through Mircera® and has deployed a dedicated nephrology salesforce, yet its core value thesis remains contingent on NMPA approval of AP301 and the subsequent commercial ramp. Net IPO proceeds of approximately HK$1.181 billion are expected to fund existing clinical programs through multiple anticipated inflection points, though commercial-scale expansion following AP301 approval may require incremental capital deployment.

Catalysts and opportunity factors include: (i) AP301 NMPA NDA approval, which would represent the first oral iron-based phosphate binder approved in China and an immediate commercial inflection for the company; (ii) NMPA Breakthrough Therapy Designation for AP306, which confers priority review benefits that could accelerate the development timeline relative to standard review; (iii) the first-in-class positioning of AP306, AP303, and AP308, each of which presents optionality for global licensing transactions or strategic acquisition interest from large-cap pharmaceutical acquirers seeking renal pipeline exposure; (iv) the China-U.S. MRCT design for AP301, which, if successful, opens a potential FDA NDA pathway and materially expands the accessible patient population; and (v) the 103.5% first-day IPO return, which signals robust public market demand and creates a favorable re-rating backdrop as clinical milestones are delivered.

Principal risk factors include: (i) NMPA NDA review outcome and timing uncertainty for AP301 — while the Phase III primary endpoint has been met, regulatory review is a distinct risk that lies outside management control; (ii) potential divergence in efficacy or safety profiles between Chinese and non-Chinese patient cohorts in the global MRCT, which could complicate a subsequent FDA submission; (iii) proof-of-concept risk inherent in first-in-class Phase II programs (AP306, AP303, AP308), where mechanism validation has yet to be established in pivotal trial settings; (iv) competitive pressure from generic ESA alternatives and low-cost phosphate binders distributed through dialysis chains; and (v) standard HKEX biotech liquidity and currency risks associated with RMB-denominated operations and HKD-denominated equity.

AP301’s foundational intellectual property was developed within Vidasym Inc., a U.S.-based clinical-stage company co-founded by Alebund CMO Dr. Jin Tian. Alebund acquired China rights to AP301 in 2018 and global rights in 2021 from Vidasym — transactions classified in the HKEX prospectus as involving a non-independent party. While the terms were described as determined through arm’s-length negotiation, investors should independently assess the alignment between founder economic interests and company interests within this structure. Additionally, an Acting-in-Concert (AIC) agreement grants Dr. Gavin Xia casting authority in the event of disagreement among concert parties, which may structurally limit minority shareholder influence in contested governance situations.